How I Paid Off $6,000 in 6 Months (Debt Payoff Case Study)

THIS POST MAY CONTAIN AFFILIATE LINKS. MEANING I RECEIVE COMMISSIONS FOR PURCHASES MADE THROUGH THOSE LINKS, AT NO COST TO YOU. PLEASE READ MY DISCLOSURE FOR MORE INFO.

Today, I’m going to show you how I paid off over $6,000 in credit card debt in 6 months.

And I was able to bury this debt despite working full time which required extensive travel, working on repaying other debt, and still having a life.

How did I manage to pay off that debt so quickly? Using the Debt Nor’Easter Method. And in this case study I’m going to show you exactly how I did it, step by step.

How I used the Debt Nor’Easter Method to pay off $6,000 of credit card debt in 6 months.

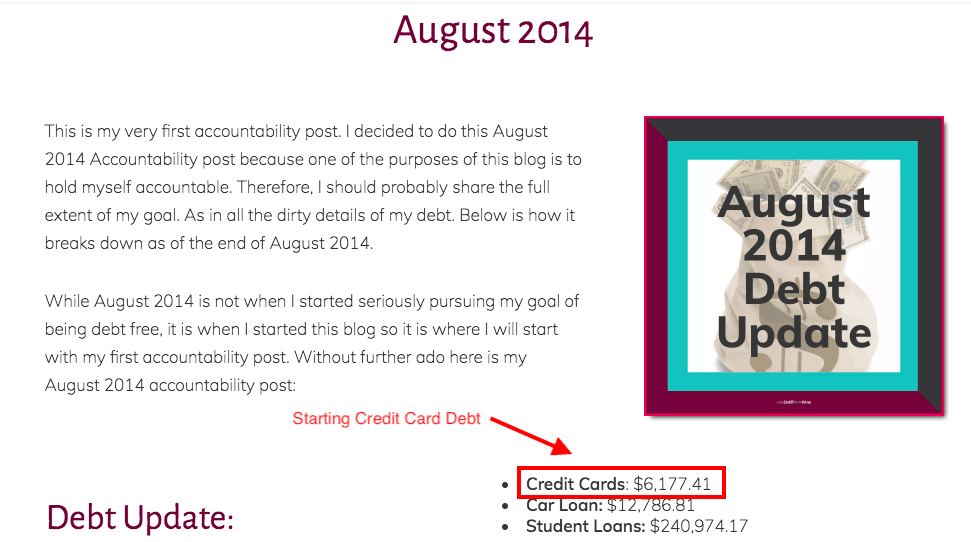

On August 20, 2014, I made a public declaration on my shiny new blog, of my intent to pay off my debt, the total stood at $6,177.41.

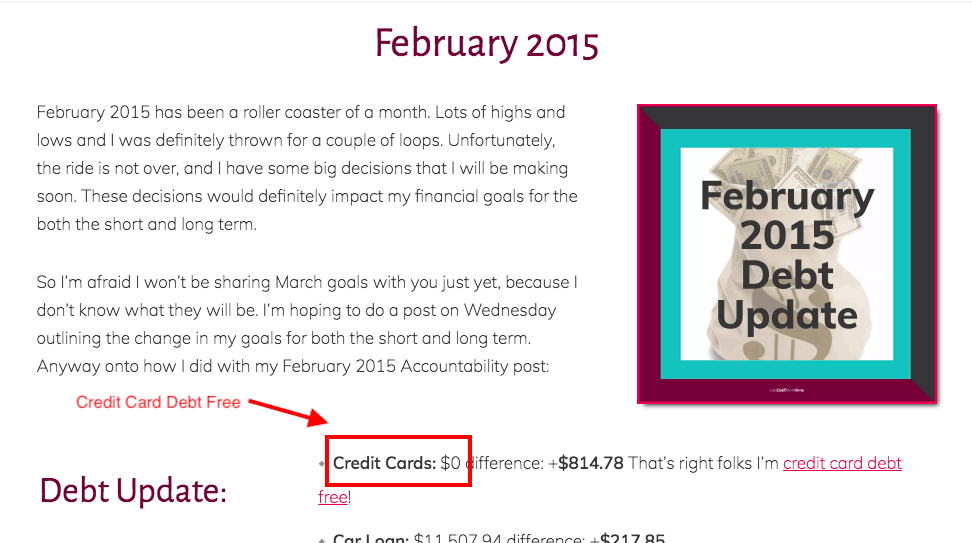

After implementing the Debt Nor’Easter Method, I managed to pay it all off by February 19, 2015.

More importantly, it freed up my money to build savings and then to make a multi-state move a month later, to be closer to family.

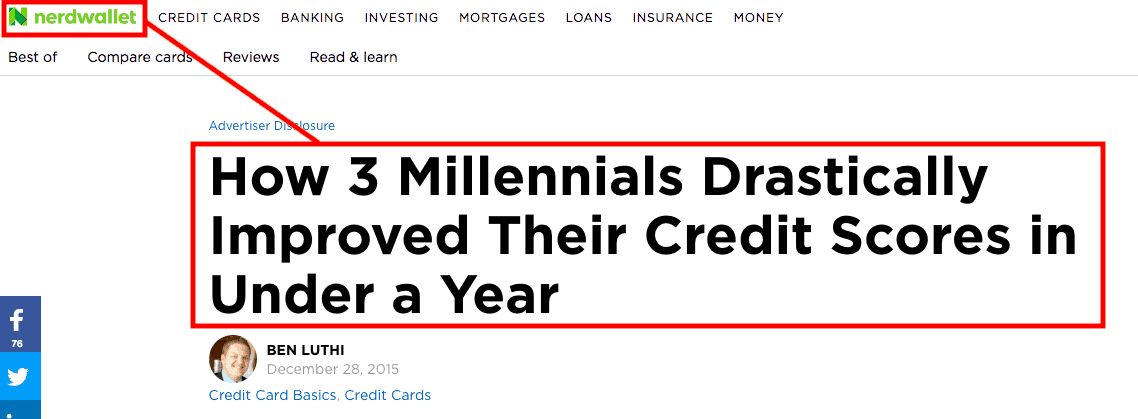

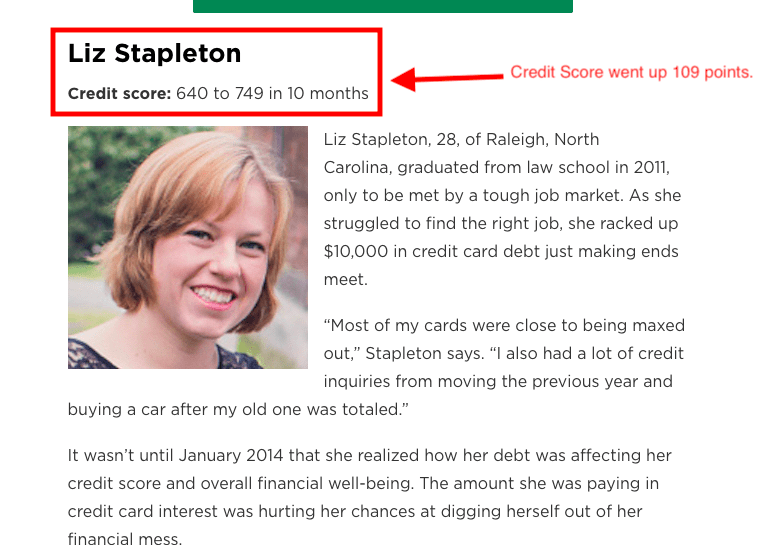

A nice bonus was that paying off that credit card debt seriously boosted my credit score (by more than 100 points), allowing me to qualify for a smaller deposit on my new apartment when I moved (and got featured in NerdWallet)

The best part? You can do the same thing, even if you’re dealing with other debt and are budgeting at your best.

The 5-Steps to Implementing the Debt Nor’Easter Method to Bury Your Debt and Improve Your Finances

There are five steps to the Debt Nor’Easter Method.

And I go over all of them in this quick video:

As I mentioned in the video above, here are the five steps that make up the Debt Nor’Easter Method:

- Stop going further into debt

- Hunker down with the numbers

- Start with saving

- Get mentally prepared to bury your debt

- Utilize snowflakes, snowballs, AND avalanches

Here is why this method works so well (and what it has to do with a Nor’Easter):

Have you ever been caught in a storm and said, “Wow, this sucks I wish it would stop!”

Of course, you have, and that is exactly how your debt is going to be feeling, because you, my friend, are going to be the storm.

Storms are powerful, they knock out power, tear down trees, cause floods, all the things you want to do to your debt (especially taking away its power).

And when shit is really going down, one storm finishes, only for another to roll on in. Just like when dealing with your debt, you can do tons of damage to it, take a breather and come back and hit it again.

Step #1 Stop going further into debt

Trying to pay off debt, while you’re still going into debt is like pushing a rock uphill. It doesn’t work very well and you may end up further behind than when you started.

“Stop going into debt” is easier said than done, especially when your computer remembers your credit card information.

If your credit cards are part of your debt problem you need to delete that information from your computer so it doesn’t autofill. You also need to stop carrying around your credit cards.

Stop Credit Card Autofill on Your Computer So You Won’t Be So Easily Tempted to Spend

To do this you need to delete that information and prevent it from auto-filling on your computer, here’s how:

Clearing Credit Card Information on Chrome:

In the top right and corner, click the gear or three dots, then select settings.

Scroll to the bottom of the page and click on Advanced.

Go to the Password section and then autofill settings.

Click the three dots and select copy, follow the link and then click Remove on the credit card.

Then back in settings you may choose to turn autofill off.

Here is a short video to show you how to delete your credit card from autofill in Chrome:

Clearing Credit Card Information on Safari:

Click Safari in the top left hand corner.

Select Preferences.

Go to Autofill.

Next to Credit Card, select Edit.

Select the credit card and hit Remove. Then click Done.

Then uncheck the box next to Credit Card.

Here is a short video demonstrating:

Stop Carrying Around Your Credit Cards So You Can Prioritize Your Spending

You also need to stop carrying around your credit cards.

Literally, go to your wallet and take all of them out.

Put all but one of them somewhere safe.

I’m a woman so I have wallets and purses I’m not using right now and I just put them in there. If you’re a dude, might I suggest your underwear drawer? Or if you have a safe or lockbox even better.

If you really can’t trust yourself with them, cut them up.

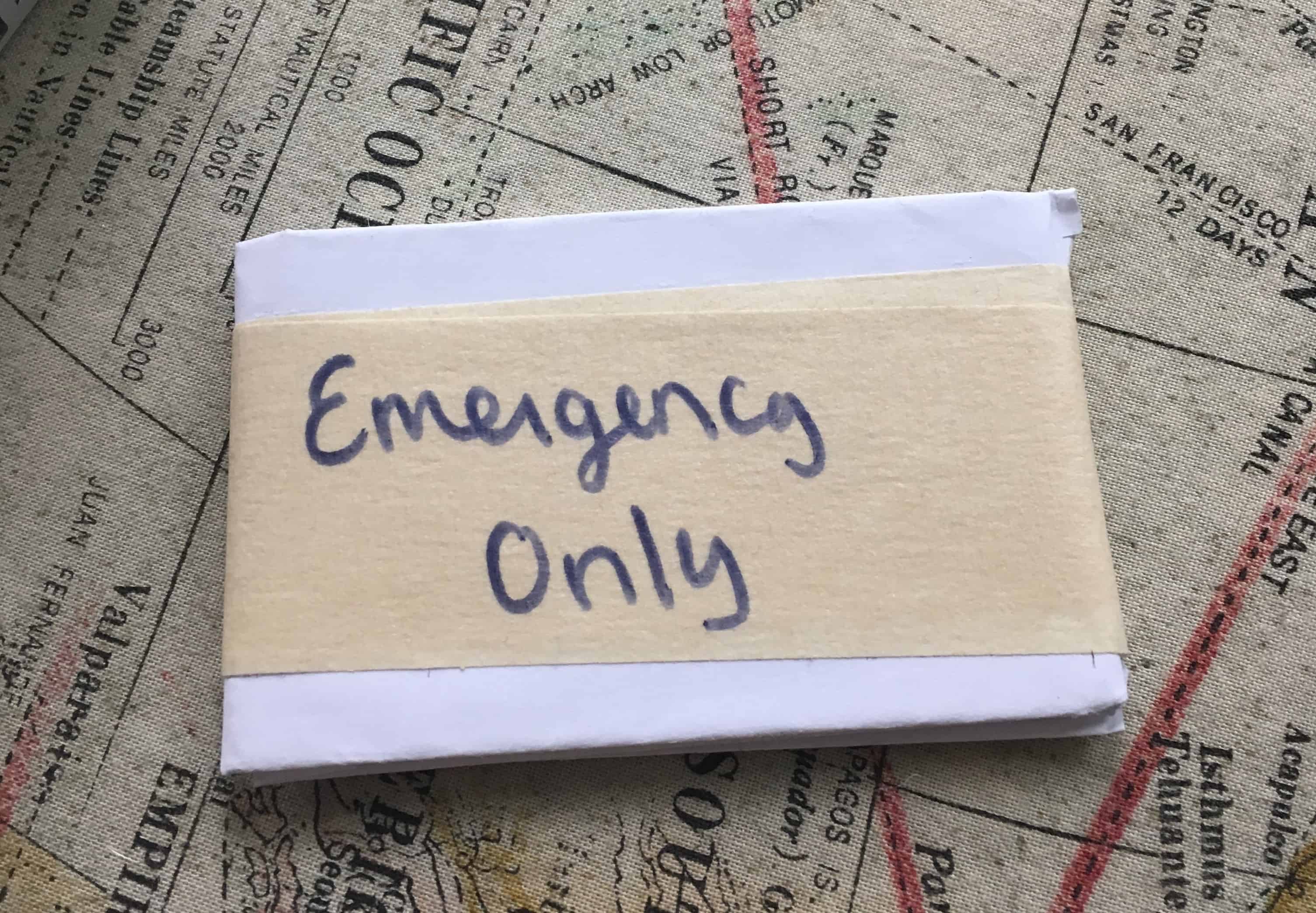

Now, I know what you’re thinking, you might need one for emergencies. That is what the one you didn’t put in the safe place is for, however, before you put it back in your wallet you need to do something first.

Wrap it in paper and write: Emergencies ONLY!!! on it. Then wrap it in tape, so that you would be embarrassed to unwrap it for anything but an emergency.

Quickly, here is a reminder of an emergency:

Emergencies:

- Any situation where you end up in the hospital

- Your car breaks down and it needs to be towed

- Your dog ate a raw pizza dough and has to go to the emergency vet (true story)

Not emergencies:

- Take out coffee because you overslept (drink the shitty free stuff at the office)

- Groceries because you’re over budget (look in your pantry)

- A concert (even if it is Beyonce)

Don’t Take Out Any New Loans or Credit Cards To Make Step #2 Even Easier

Obviously, new loans or credit cards would qualify as new debt, and this first step is for you to stop going into debt, so don’t take out new loans or credit cards. Kapish?

The one exception is if you are able to refinance one of your loans for a lower rate, so you’re essentially replacing the loan rather than adding another loan to the list.

Step #2 Hunker Down with the Numbers

To prepare for the Debt Nor’Easter storm you’re going to need to gather supplies, I recommend wine.

Now, sit down with your bottle of wine and on one page write out every single debt you have. Include:

- Name of the debt. Is it a car loan, is it a student loan? From undergrad or graduate school. Is it a credit card what company is it with? Write it down.

- Current balance. What is your balance as of today. Go look it up, don’t look at your last statement balance. Actually log into your account and find out the current payoff balance.

- Interest rate. What is the interest rate for the debt, don’t do an estimate or round it up or down. Go look it up. If it’s 14.99%, don’t write 15%, write 14.99%.

- Maturity date. This is how long it will take to pay off if you stick to the minimum payment. Your credit card statement will usually include a table like the one shown below outlining how long it will take you to payoff the current balance and the amount of interest you would pay. With other debt like a car loan, the maturity date is the end of the loan term. So if you you took out a 6-year car loan on January 1, 2014, the maturity date is six years from the start of the loan, so January 1, 2020.

- Minimum monthly payment. How much are you required to pay every month no matter what, write it down.

You can gather all of this information on any sheet of paper:

Once you’ve got it all written down, it’s time to total up.

Add up every single balance to get the total amount of debt you owe.

Next add up all of the minimum payments, to get the total minimum amount you have to pay each month. You’ll need this list when you get to step 5 of the Debt Nor’Easter method.

Step #3 Start with Saving

You have stopped gaining more debt which is great. But to make sure it stays that way while you work to pay off your debt you need to have some savings.

Savings means that when the unexpected comes up or an emergency, you can pay for it without having to take on more debt. I’m now going to show you how you can save money even when you feel like it’s impossible.

First, to ensure you aren’t unnecessarily spending your savings you need to have a place to put that money. You can open a savings account with your current bank or another bank, or you can do what I now do and use an app.

How to Save with Qapital

I use the Qapital App to both help me save and give me somewhere to put those savings.

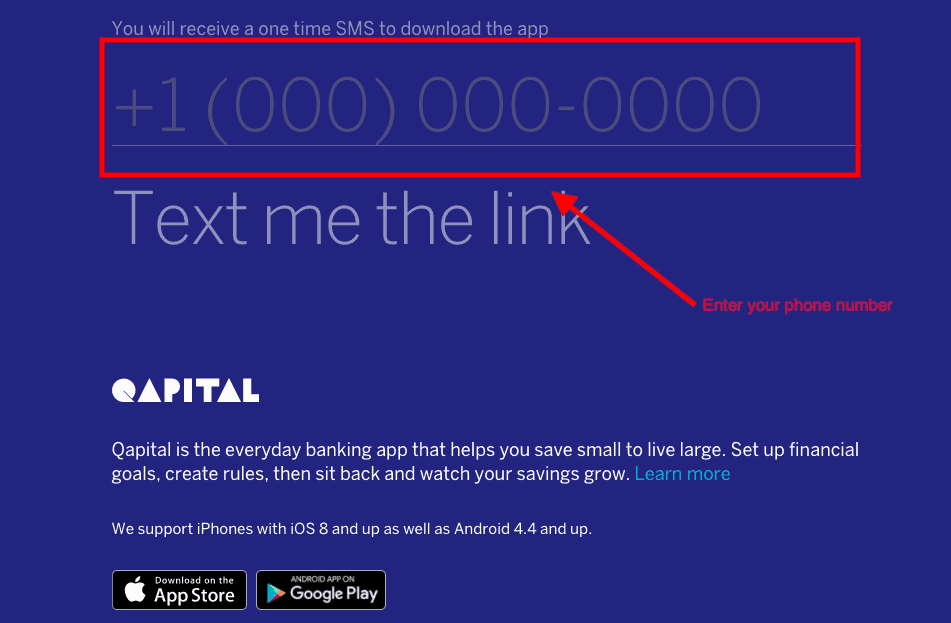

To get started with Qapital, click this link.

Next, enter your phone number.

Qapital will text you the download link.

Download the app then sign up using your email or Facebook.

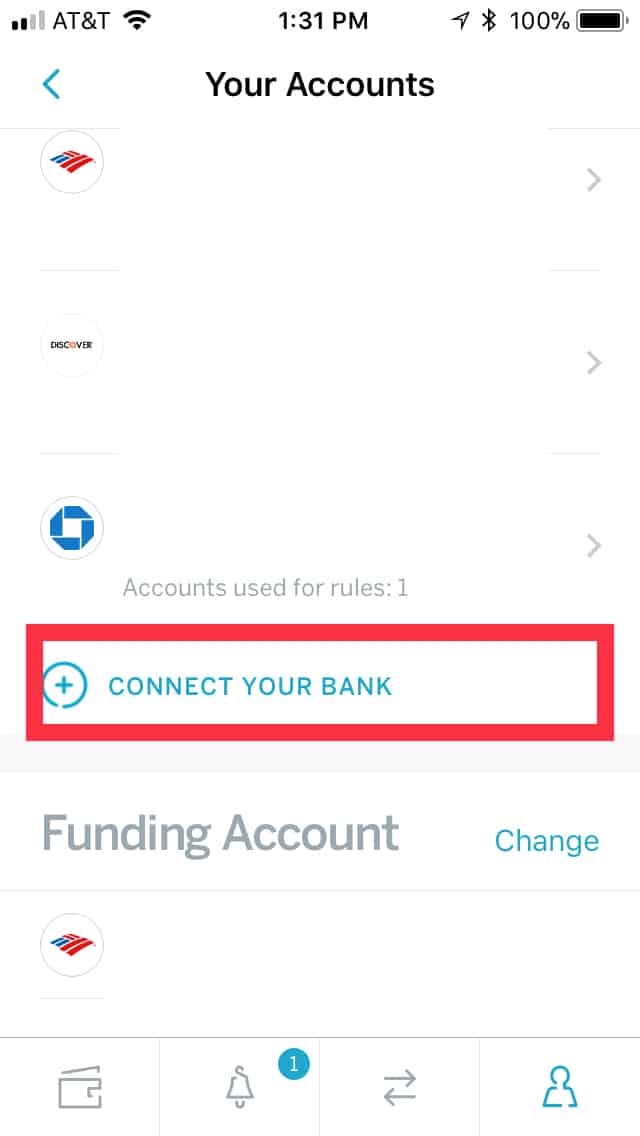

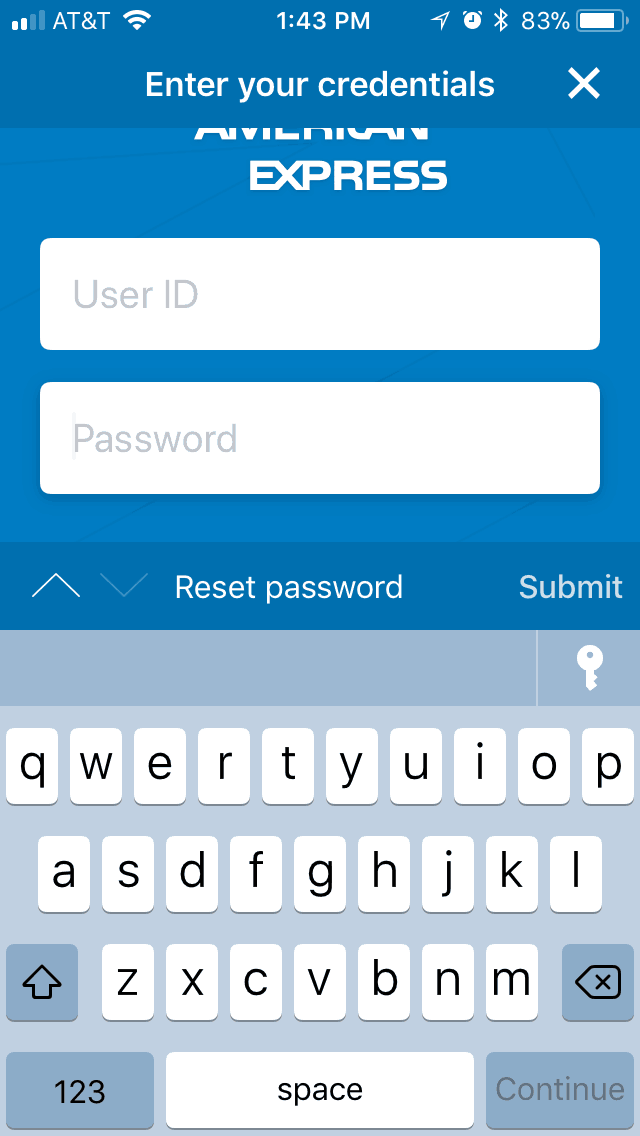

Next you need to add your bank account, by clicking: Connect Your Bank

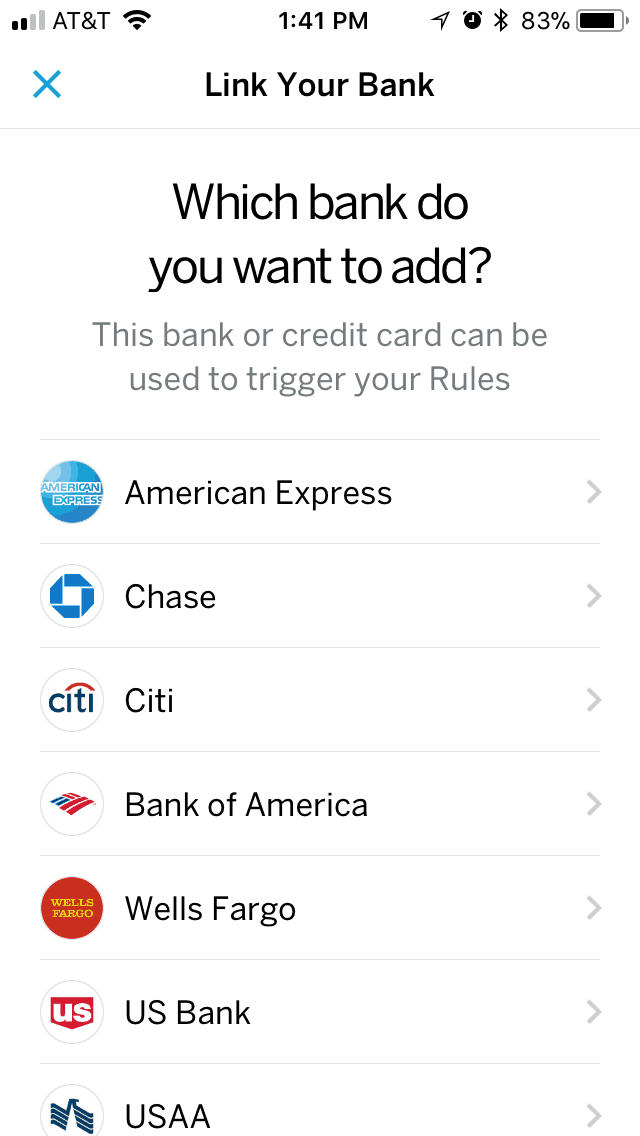

Choose the bank from the list provided.

Enter your bank login credentials to get it connected.

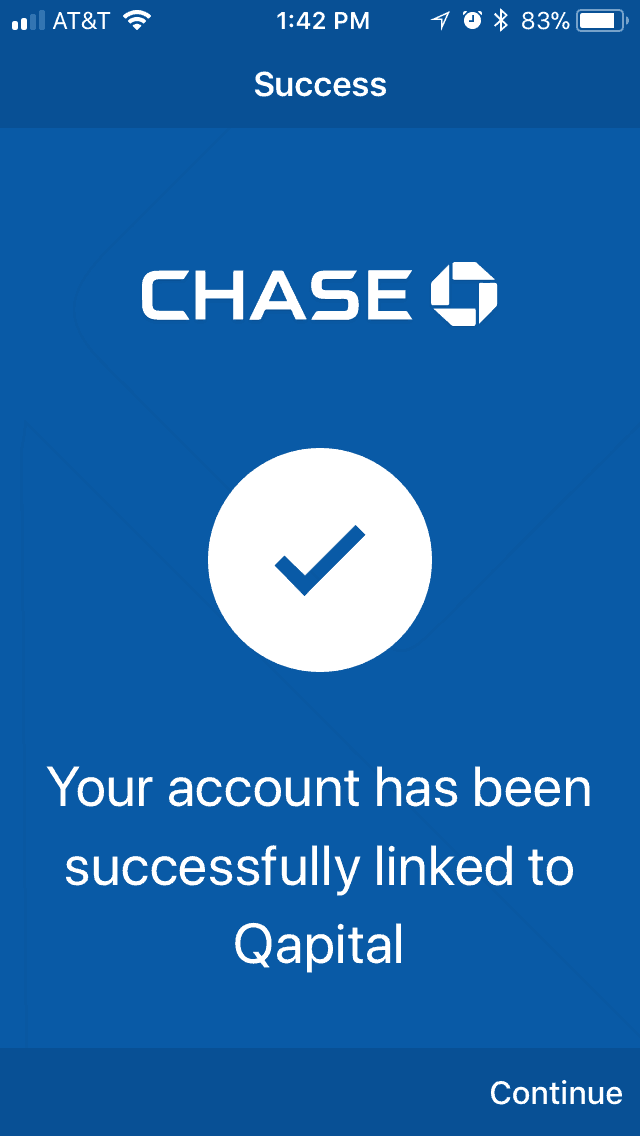

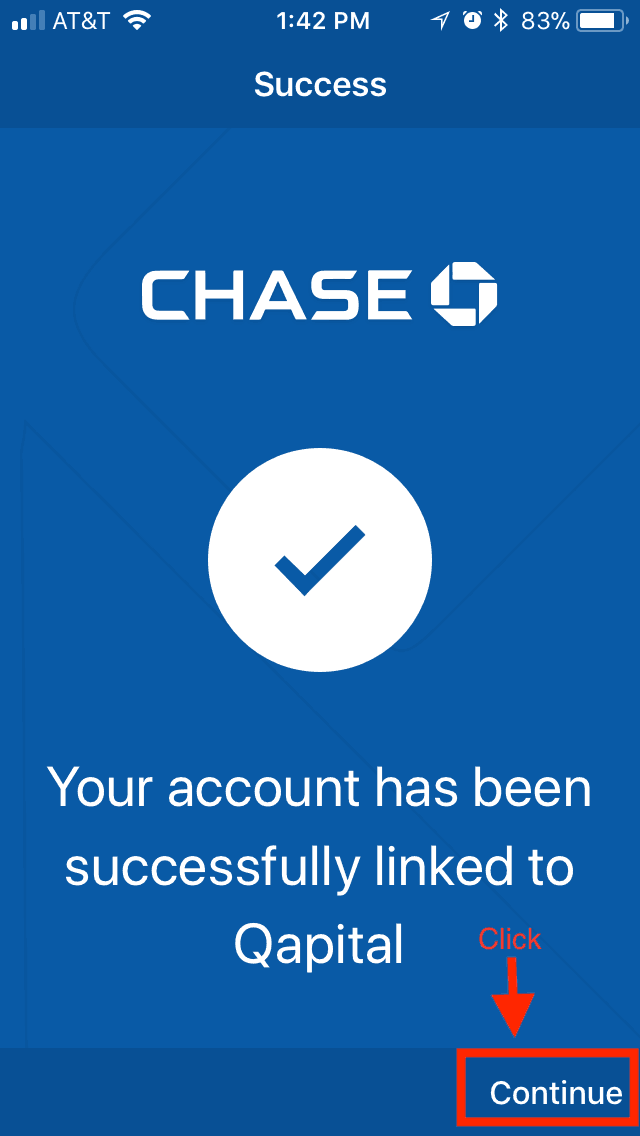

You should see a success message.

Click continue.

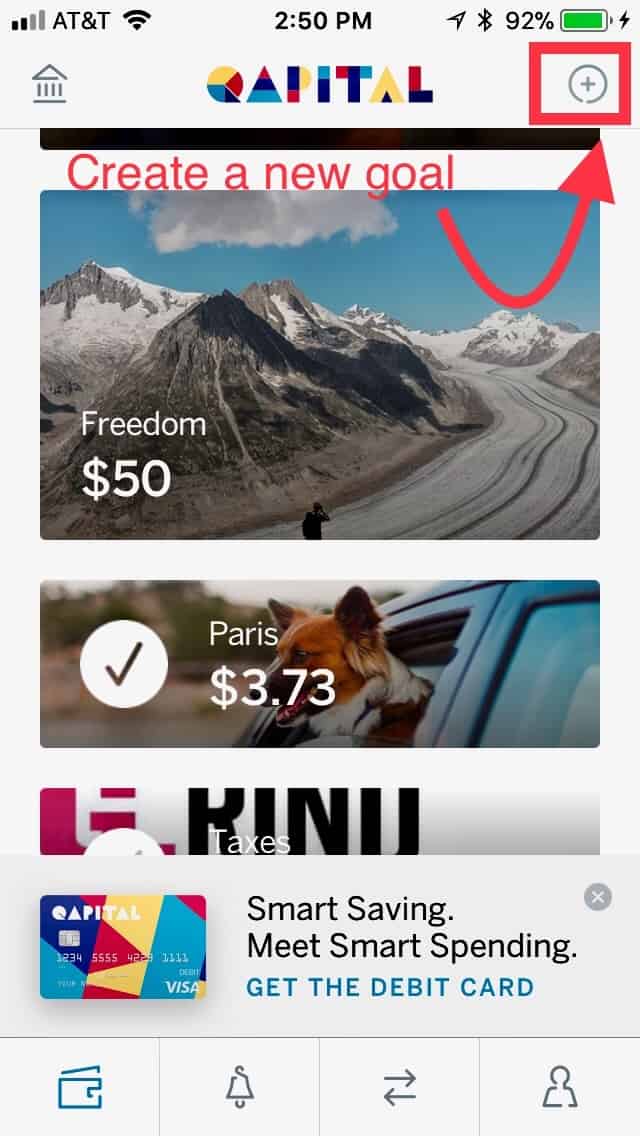

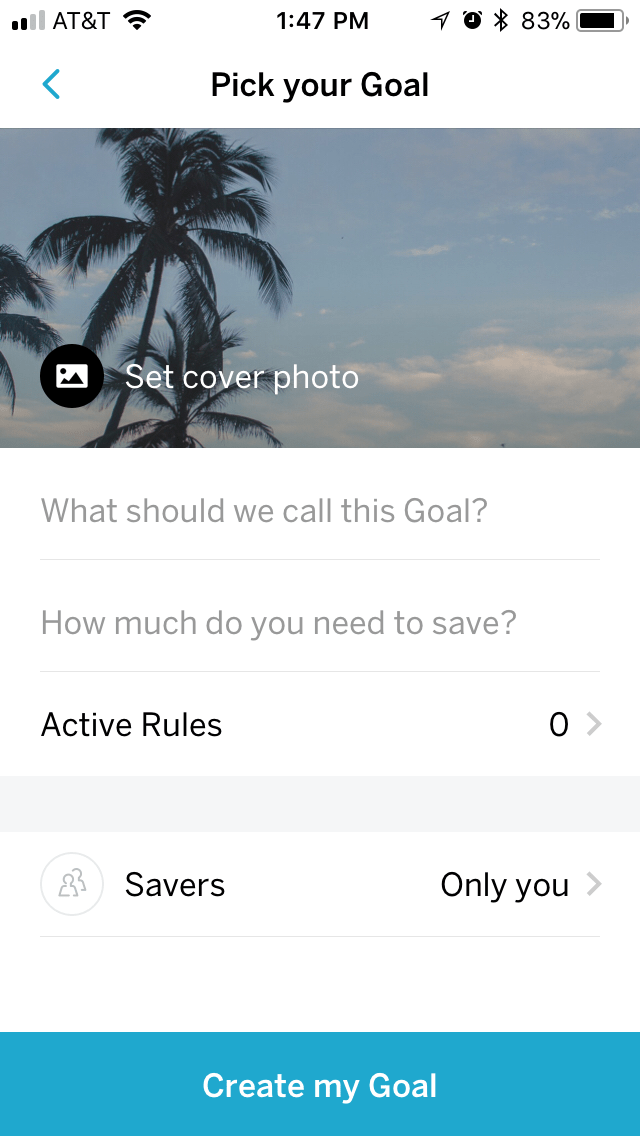

You are now ready to set up your first savings goal.

The really cool thing about Qapital is that it helps you to automate saving according to YOUR rules.

Yes, it lets you easily do the 52 week savings challenge, but you can also set a rule to save every time you splurge on Dominos. Or round up every purchase to the nearest $2 and putting that spare change towards your savings.

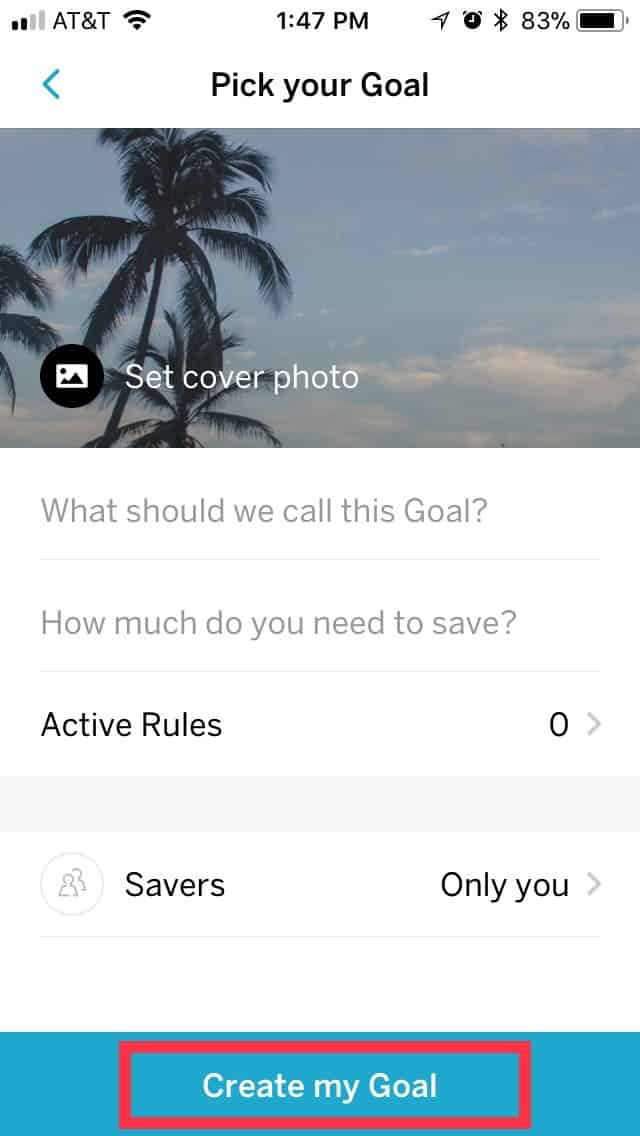

To create a goal:

Select the plus sign next to “Create a Goal”

Next, decide why you are saving, I suggest going with “Just Start Saving” at the bottom. But if you want to get specific you can select “Something Else” and Title it however you want.

Name your goal, I suggest using Debt Payoff Safetynet

Decide how much you need to save, I recommend setting a goal of 3x your last emergency.

For example, if your last emergency cost you $800, your savings goal will be $2,400.

If putting an amount that large is intimidating, start with something smaller, you can always raise your goal later.

If you want to spice up your goal, you can set a cover photo, I think this one that Terry Crews uses of Terry Crews is perfect.

It’s a great reminder not to spend that money unless you really have too, Terry Crews is judging your spending.

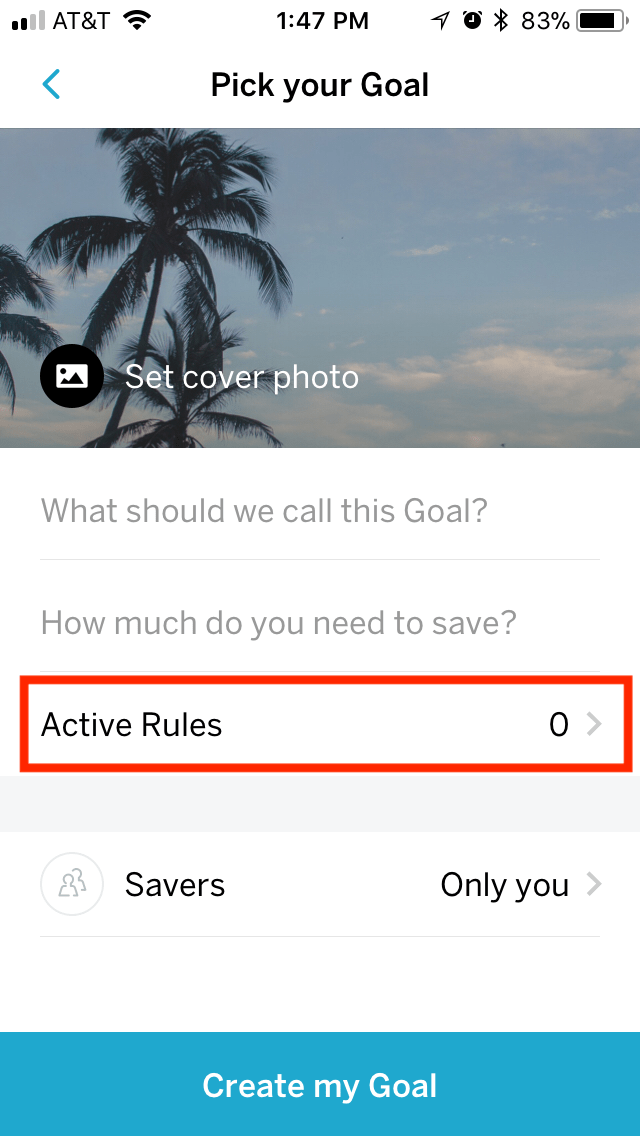

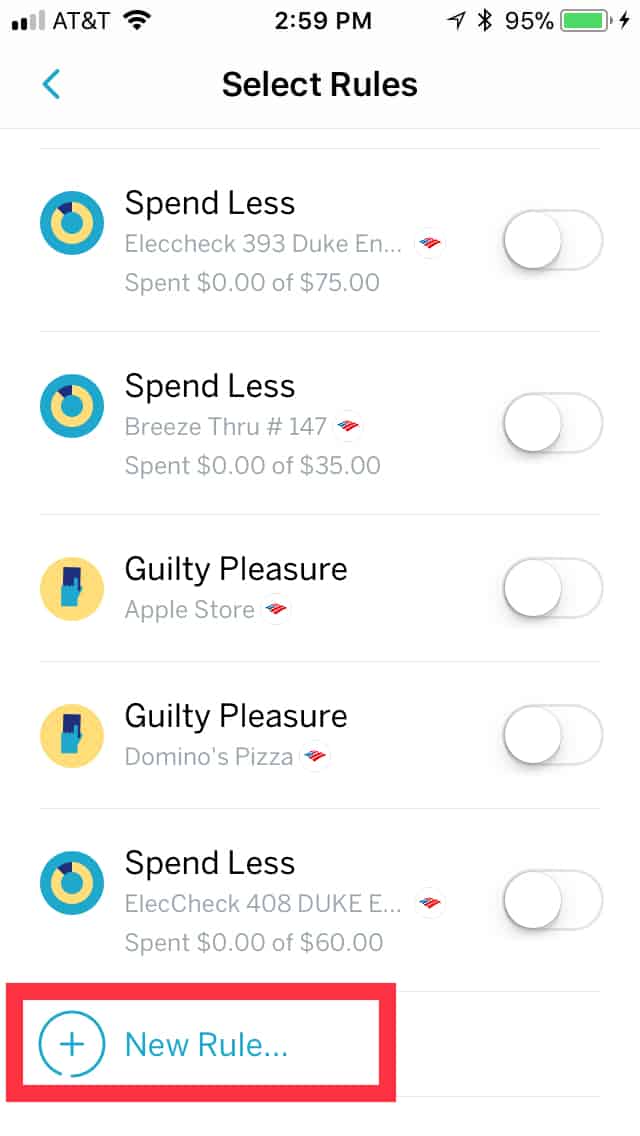

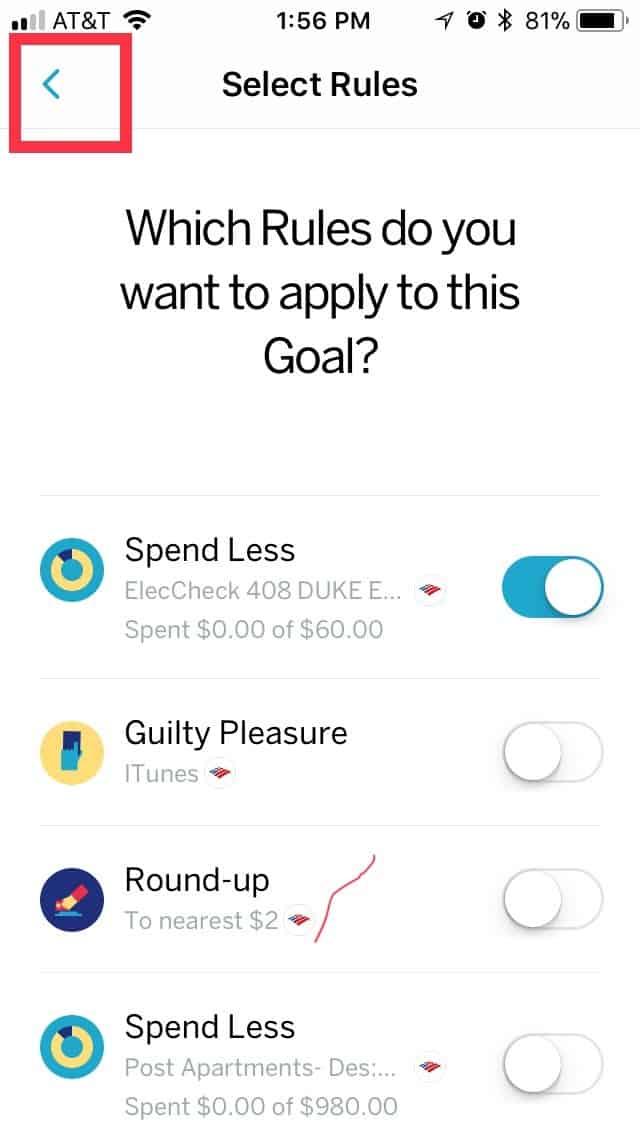

Now comes the really fun part, creating your savings rules.

Click on Active Rules.

Then scroll down and click New Rule

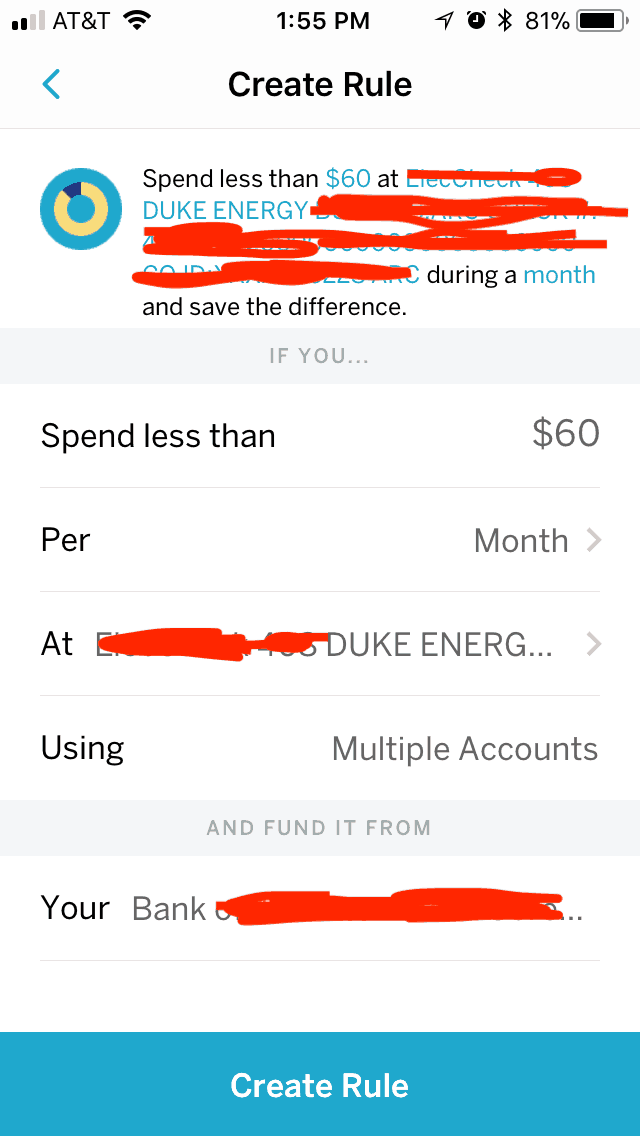

I like the spend less rule.

It allows you to set a budget and if you come in under budget it saves the remainder. I like to do this for my electric bill since it varies by month. Meaning I can budget a flat rate and whatever gets left, actually gets saved.

Once you’ve decided your budget amount it will be the amount you “Spend less than”

I choose per month because it’s a monthly bill

I then go select the Merchant.

Finally, just click create rule.

Click the arrow back to the Goal Set up Page.

Finally, hit Create My Goal.

You’ve just put your savings on autopilot, now let’s get back to destroying your debt with step #4 of the Debt Nor’Easter Method.

Step #4 Get Mentally Prepared to Be a Storm and Bury Your Debt.

Getting yourself mentally prepared means you have to make paying off your debt the first thing you do with your money.

You have likely heard the phrase:

Pay yourself first.

When learning about personal finance, what it means is pay your goals first. We’ve already set your savings on autopilot, now it’s time to make paying off debt your number one goal.

A mistake too many people make is planning to put whatever is left over at the end of the month as extra towards your debt. The problem is there is usually nothing left.

To prioritize debt repayment, you need to budget and see how much you are budgeting towards your debt. Once you know the amount, make that extra payment. Do not wait until the end of the month to see if that extra money is left.

Simply put, the same day the money is made available in your account is the same day you make that extra payment towards your debt. That way you can say bye, bye, bye to your debt.

Step #5 Utilize Snowflakes, Snowballs, and Avalanches

The beauty of the Debt Nor’Easter is that it’s flexible to not only save you the most money but also keep you motivated to keep paying off your debt.

It differs from the more traditional and well-known Debt Snowball and Debt Avalanche in that you choose which debt to focus on first based on the greatest benefit once paid off.

I’ll explain further in just a bit, first let me explain the Debt Snowball and Debt Avalanche strategies.

The Debt Snowball and Debt Avalanche are common debt repayment strategies. They work like this:

The Debt Snowball Method

With the Debt Snowball you order your debts from smallest to largest. You make the minimum monthly payment on all your debts, and then you target the smallest balance with extra payments until it is paid off. You then snowball that payment into the next smallest payment.

The most common benefit of the Debt Snowball is the motivational surge you get after quickly paying off that first small debt.

The disadvantage of the Debt Snowball is that it will likely cost you more money, in terms of the amount of interest you end up paying. Which is why people will often turn to the Debt Avalanche…

The Debt Avalanche Method

With the Debt Avalanche method you order your debts based on their interest rates with the highest interest rate first. You make minimum payments on everything and put extra payments towards your highest interest rate debt until it is paid off.

The most common benefit of the Debt Avalanche is that is saves you money on interest.

The disadvantage is that it can take a while to pay off that first debt and can lead to discouragement.

The good news is that you’re an effing storm and you’re not going to let a little discouragement get in your way, because you aren’t going to use either method, you’re going to use both.

Don’t Use Either Method, Use Both

Now, there is nothing wrong with using either the Debt Snowball or Debt Avalanche method, but for someone like me, neither was really going to cut it.

Because yes my credit cards had higher interest rates than my student loans, but one of my student loans has a balance of nearly $50,000 and an interest rate of 8.5%….

This means that student loan cost me $11 in interest PER DAY.

Whereas my $2,500 credit card at 17.99% interest cost only $1.23 a day.

So paying off the highest interest rate debt doesn’t really save me money. And paying off the lowest balance when I have so much debt isn’t all that exciting either.

So instead of using either, I decided to use both along with the Debt Snowflake method (more on this in a second).

When starting to pay off my debt I was staring down credit card debt, a car loan, a bar loan, and a mountain of student loans.

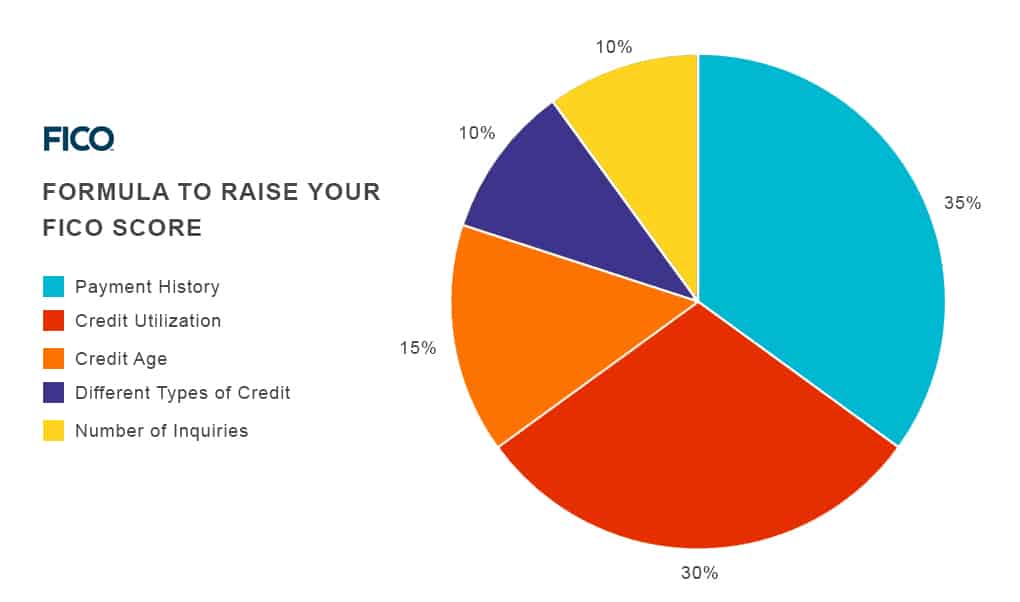

I decided to start with the credit cards first, not just because they had the highest interests (as I already demonstrated – that didn’t save me money), but because their being gone would produce the swiftest improvement to my finances (raising my credit score).

Credit cards are revolving debt (aka credit utilization) and have a HUGE (30%) impact on your credit score, by focusing on them first I could get myself on better financial footing to pay off the rest of my debt.

Via Credit Sesame https://www.creditsesame.com/blog/credit/improve-your-credit-score/

Having already paid off the smallest balance credit card, before I knew what the Debt Snowball was, but implementing it nonetheless, I was left with three credit cards to pay off.

Having already knocked my debt down a notch with the snowball, I hit is simultaneously with the Debt Avalanche and Debt Snowflake methods.

I started focusing on the credit card that had the highest interest rate and my extra payments went towards it first.

Then throughout the month, any extra money I made, be it a side hustle gig, or a rebate I cashed in, that money went directly to paying off that credit card. This is referred to as the Debt Snowflake Method. All those small amounts added up, like a bunch of little snowflakes totaling three feet of snow.

Once it was paid off, I took a bit of a breather and then I went in for round two and buried that second credit card and then finally the third.

Prioritize Your Debt Types By The Benefit You’ll Get Having Them Paid Off

Now, go pull out that list of debts you put together in Step 2.

When you’re looking at what debt to tackle first, determine which one, when paid off, will provide you with the most benefit.

After paying off my credit cards, I started focusing on my car loan, even though it was the lowest interest rate debt and one of the lowest balances too.

I did this because if something were to happen to the car before it was paid off, I’d be totally screwed, I couldn’t afford to be underwater on my car loan (i.e. owe more than it’s worth).

Once you know which debt you will bury first, go after it with everything you’ve got, snowballs, avalanches, and snowflakes, make it give you a terrible name, because you’re that bad of a storm. So I decided to prioritize it.

It doesn’t really matter which method you lean on more, just so long as you stick with it through that particular debt.

And I do mean particular debt, not debt type.

For example, if you want to go back and forth between your lowest balance credit card then highest interest rate, then next lowest balance, etc. go for it.

The more excited you are to crush and bury that debt the easier it will be to actually utilize all the various snow-related methods in your belt to create a Debt Nor’Easter.

Wrapping it Up

So that is how you destroy debt with the Debt Nor’easter Method. Unlike the Debt Snowball or Debt avalanche, you don’t have to focus on any one method and it will still save you money and stress.

If you plan on destroying debt this month, let me know in the comments below!

Frequently Asked Questions

If you still have questions about how to pay off 6000 in debt, we’ve answered the most common questions below.

How Much Credit Card Debt is Too Much?

There isn’t a specific answer to this question, as it varies from person to person. However, if you’re unable to make your monthly payments, are constantly being hit with late fees and interest charges, or are using credit cards to pay for everyday expenses, then you likely have too much credit card debt.

What to do after you escape credit card debt

When you finally pay off your last credit card, celebrate! You’ve worked hard and now it’s time to enjoy the fruits of your labor. But don’t stop there, continue on with your debt-destroying ways and knock out the rest of your debts for good. Here are four tips to help you stay motivated and on track:

1. Set new goals. Celebrate your victory by setting new goals for yourself, such as becoming debt-free within a certain amount of time or saving up a down payment for a house.

2. Stay disciplined. Just because you’ve paid off one debt doesn’t mean you can slack off on payments or start spending money recklessly. Stay disciplined and keep making extra payments towards your remaining debts until they are all gone.

3. Reward yourself along the way. As you make progress in paying off your debts, treat yourself to something special—but be sure to stick to your budget!

4. Don’t go back to old habits. One of the biggest dangers after paying off credit card debt is going back to old spending habits that got you into trouble in the first place.

How to pay less interest

If you’re struggling to make your credit card payments, you may want to reach out to your credit card company for help. Many credit card companies offer assistance programs that can lower your interest rates, waive late fees, or even temporarily reduce or suspend your payments.

To request help from your credit card company, contact your credit card company and explain your financial situation.

Be honest about how much you can afford to pay each month.

Request a lower interest rate, or ask for a temporary suspension of payments.

If the credit card company is unwilling to work with you, consider transferring your balance to a 0% APR Balance transfer credit card or get a debt consolidation loan.

Is it worth paying off credit card debt

The answer to this question depends on a few factors, such as the interest rate you’re paying on your debt, the amount of debt you have, and your financial goals.

If you’re only making the minimum payments on your credit cards, it’s likely that much of your payment is going towards interest charges rather than the principal.

If you’re trying to decide whether or not to pay off your credit card debt, use a credit card debt calculator to figure out how long it will take you to pay off your debt if you only make the minimum payments.

Enter in your credit card balance, interest rate, and monthly payment. The calculator will then tell you how long it will take to pay off your debt and how much interest you’ll end up paying.

If your credit card debt is impacting your credit score, then it’s usually worth paying off to save money down the road with lower interest rate mortgages, car loans, and other financial accounts that determine rates using your credit score.

credit card debt calculator

Our favorite credit card debt calculator is unbury.me, but if you have a family or partner, then unbury.us is also a fantasic option.

What are the options to pay off a high-interest 17k credit card debt

You could consider using a balance transfer credit card. These cards usually offer a 0%APR for a certain amount of time anywhere from 6-24 months.

But you’ll want to make sure you are able to pay off the balance transfer in that time or interest will retroactively apply.

You’ll also want to take into account a balance transfer fee, these are usually 3-5% of the amount you put on the balance transfer card.

What will happen if/when my credit card interest pushes my debt past my credit limit

You’ll likely incur penalties or fines for exceeding your credit limit. Each approved transaction that is over the credit limit, is likely to be subject to a fee.

Read the reviews about the Qapital app they are horrible. Not too keen on using a app that charges you money for saving money.

Hey Bobby, Qapital used to be free. But the fact that it makes saving so easy, for me, it’s worth it.