How to Rebuild Your Credit After a Setback: A Practical Guide

THIS POST MAY CONTAIN AFFILIATE LINKS. MEANING I RECEIVE COMMISSIONS FOR PURCHASES MADE THROUGH THOSE LINKS, AT NO COST TO YOU. PLEASE READ MY DISCLOSURE FOR MORE INFO.

Life happens, and sometimes even the most responsible people can take a hit to their credit, through no real fault of their own.

You can budget wisely, pay your bills on time, and still find yourself in trouble.

My friend is a perfect example. She had her credit card set to autopay, thinking everything was under control. But the system tried to pull money from the wrong account. When the payment failed, her credit card company immediately shut the account down and reported a missed payment to the credit bureaus. Her credit score dropped, fast—and all because of a glitch she didn’t see coming and had no control over.

Stories like hers are more common than you might think. And if it’s happened to you, know this: you’re not alone, and you’re not without options.

As a personal finance writer with over a decade of experience, I’ve seen how easily credit problems can sneak up—and how you can bounce back .

In today’s post, I’ll walk you through how to:

- Understand what happened to your credit

- Take action to stop further damage

- Rebuild your score with smart, doable steps

Let’s take the stress out of the unknown and replace it with a clear plan to move forward.

Understanding the Impact of a Credit Setback

Credit setbacks can sneak up in everyday life. You might miss a payment, carry a high balance, or have a credit card closed—sometimes without warning. These common issues can hurt your credit score quickly.

Even one missed payment can stay on your report for years. A closed account can shrink your available credit, raising your utilization ratio. And high balances? They make you look riskier to lenders.

How Your Credit Score Is Calculated

To understand the potential damage, it helps to know how your credit score is built:

- Payment History – Do you pay on time? (35% of your score)

- Credit Utilization – How much of your credit are you using? (30%)

- Length of Credit History – How long have your accounts been open? (15%)

- Credit Mix – Do you use both credit cards and loans? (10%)

- New Credit – Have you applied for a lot of new credit recently? (10%)

When something goes wrong—like a missed payment or a closed account—it can hit multiple areas at once.

Your credit score reflects how risky you are to lenders. One misstep can send the wrong message.

The Domino Effect on Your Financial Life

A credit setback isn’t just a number. It can lead to:

- Higher interest rates on credit cards or loans

- Loan applications getting denied

- Lower credit limits on your existing cards

And the effects aren’t just financial. Many people feel embarrassed or anxious, even if the issue wasn’t their fault. It’s easy to lose confidence when your score drops.

But the good news is that knowing the impact is the first step in taking back control.

Real-Life Example: When Autopay Goes Wrong

Auto-pay can be a great tool, when it works. But when it fails, the damage can be quick and painful.

Take the example of my friend earlier, autopay didn’t work correctly and her credit score took a hard hit in more ways than one—all without warning and through no fault of her own.

Unfortunately, she’s not alone. One Reddit user shared a similar story. They had plenty of money in their bank account, but Target claimed a payment was returned due to “non-sufficient funds.” Later, Target said the account “didn’t exist.” The same bank info was used later for a successful payment, and their bank confirmed no payment was even attempted the first time. Still, Target shut down the account and reported it to the credit bureaus—without so much as a heads-up.

“Because of the returned payment that was Target’s own fault, they are cancelling my account entirely and reporting it to credit bureaus. Not a phone call or any ‘warning’ and it was their own mistake.” – Reddit user

These stories highlight just how easily technical glitches can become financial disasters. When systems fail, the fallout lands on your credit report—not on the company that made the mistake.

Immediate Steps to Take After a Credit Setback

A drop in your credit score can feel overwhelming. But the sooner you act, the more control you’ll regain. Here’s where to start:

Review Your Credit Reports

Your first step is to figure out exactly what changed. Get a copy of your credit report from all three major bureaus—Experian, Equifax, and TransUnion. You can request them for free once a year from AnnualCreditReport.com.

Look for:

- Missed or late payments

- Closed accounts

- New accounts or activity you don’t recognize

You can also use free tools like Credit Karma to keep tabs on your score and get alerts when something changes. It won’t show everything, but it’s great for spotting red flags fast.

Dispute Any Errors

If you see something wrong, take action. Dispute errors directly with the credit bureau online or by mail. The Consumer Financial Protection Bureau (CFPB) offers a detailed guide here: How to dispute an error on your credit report.

Here’s what you’ll need:

- A short, clear explanation of the mistake

- Copies of any supporting documents (e.g., bank statements or emails)

- Screenshots or proof if the issue was a technical glitch

Keep copies of all communication and follow up if you don’t hear back in 30 days.

Contact Creditors Directly

If a creditor reported the problem, don’t hesitate to contact them. You may be able to:

- Negotiate a payment plan

- Request a goodwill adjustment (especially for a one-time issue)

Be honest and calm. Explain what happened, especially if it wasn’t your fault. Many creditors are willing to work with customers who reach out.

“You can’t fix what you don’t face. Start small—one call or one report at a time—and momentum will build.”

Strategies to Rebuild Your Credit

Once you figure out what happened to mess with your credit, it’s time to take action to rebuild your credit. While we’d all love to rapidly fix everything, the truth is slow and steady is what works. With consistent effort and a smart plan, you can raise your score and regain financial confidence.

Build a Positive Payment History

Since Payment history makes up the biggest part of your credit score, this is a great place to focus first.

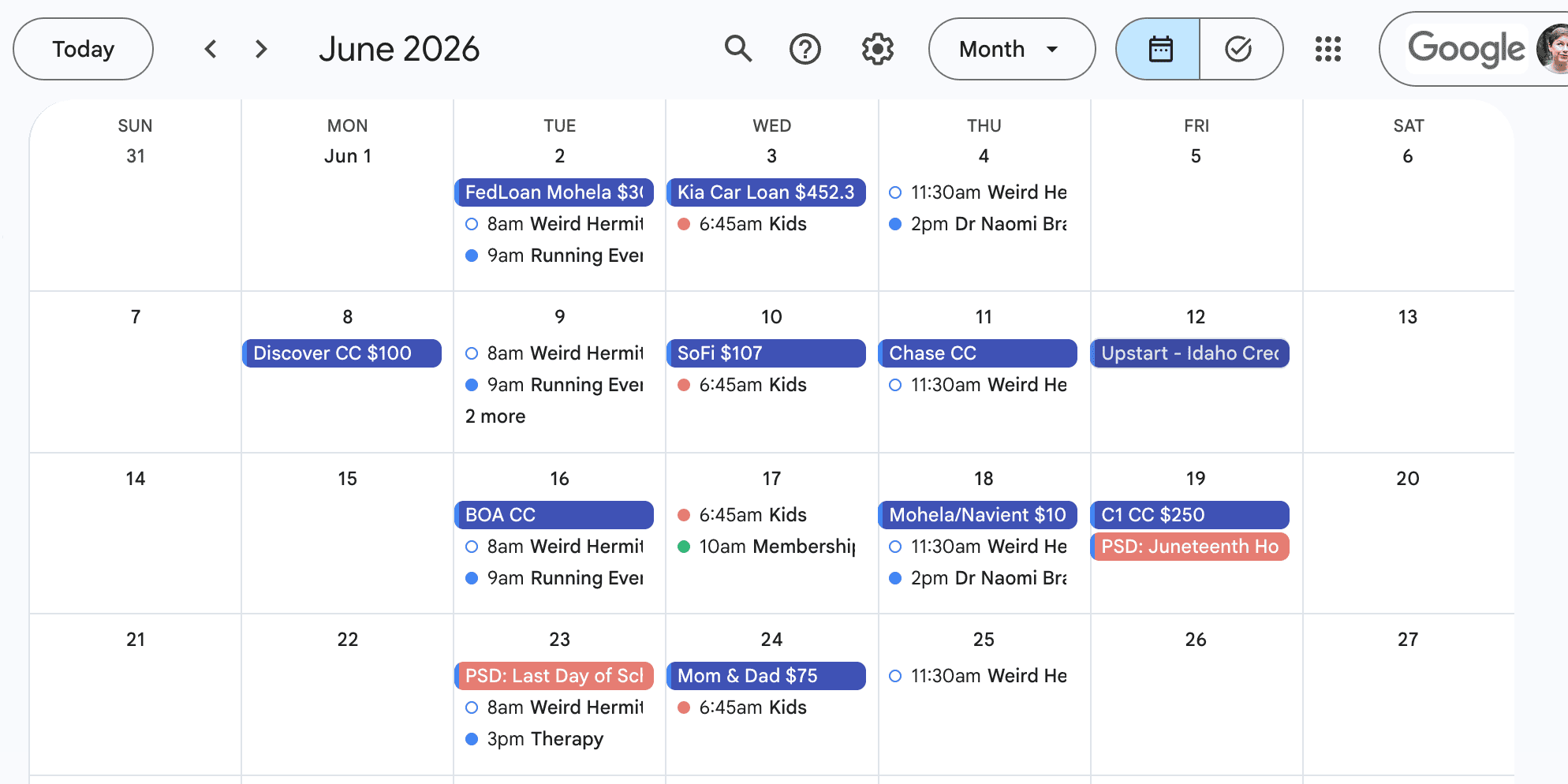

- Set up payment reminders in your calendar or budgeting app. I like to do recurring events in my calendar and add a check emoji when it’s been paid:

- Use autopay wisely, and double-check your account links to avoid past issues. Personally I like to automate savings, but keep debt repayment fairly manual so I stay on top of everything.

- Consider secured credit cards if your current accounts are limited.These cards are designed to help you build/rebuild credit, not trap you in fees. Just be sure to pay the balance in full each month.

Manage Your Credit Utilization

Try to use less than 30% of your available credit. Lower is better.

If your credit limits were reduced due to the setback, don’t panic. One smart move: call your credit card company and ask them to restore your old limit. Explain what happened. If you’ve resolved the issue and your record was solid before, they may say yes.

The worst they can do is say no, and you’ll still have taken a step to advocate for yourself. Even if that doesn’t work there are other steps you can take:

- Pay down high balances strategically (start with the card closest to its limit).

- If possible look into a credit consolidation loan, even if the interest rate is high, such as 15% that is likely still lower than you current credit card interest rates

- Consider a balance transfer to help pay down balances faster – but be wary while many of these will offer 0% interest, if you don’t pay off the balance by the end of the promotional window, the high interest rate can be retroactive. Be sure you fully understand the terms before doing a 0% balance transfer.

Tools and Resources to Aid in Credit Recovery

Rebuilding your credit is easier when you’ve got the right tools. These resources can help you track your progress, stay organized, and keep learning as you go.

Credit Monitoring Services

Keeping tabs on your credit is essential, especially after a setback. These tools let you catch issues early and watch your score improve over time:

- Credit Karma – Free credit score monitoring, alerts, and personalized tips.

- Experian – Offers real-time score tracking and the ability to boost your score using on-time utility and streaming payments.

Many of these services will also alert you to new accounts or changes to your credit report.

Budgeting Tools

Strong money management supports credit recovery. These tools help you plan your spending and make sure bills get paid on time:

- YNAB (You Need a Budget) – A proactive budgeting tool that helps you give every dollar a job. Great for staying on top of payments.

- Rocket Money – Helps you find and cancel unused subscriptions, track spending, and set financial goals.

Using a budgeting app takes the guesswork out of staying on top of bills, especially when life gets busy.

Preventing Future Credit Setbacks

Once you’ve started rebuilding, the goal is to stay on solid ground. A few smart habits can protect your progress and help you avoid surprises down the road.

Do Regular Financial Check-Ups

Just like your health, your finances need regular check-ins. Set aside time each week to review:

- Your bank and credit card accounts

- Upcoming bill due dates

- Any changes to your credit report

One simple tool: a personal finance calendar. Mark all your bill due dates, paydays, and auto-draft charges. You can use a paper calendar, Google Calendar, or a budgeting app. This makes it easy to stay ahead of deadlines and avoid missed payments.

You can also set reminders for quarterly reviews—like checking your credit reports or rebalancing your budget.

Frequently Asked Questions

How long does it take to rebuild credit?

It depends on your starting point and how consistent you are. If you take steady steps, like paying bills on time and lowering credit card balances, you might see improvement in a few months. But rebuilding fully can take 12 to 24 months or more, especially after serious setbacks.

Keep in mind: credit repair is a marathon, not a sprint. Focus on progress, not perfection.

Can closed accounts be removed from credit reports?

Not usually. If the information is accurate, closed accounts will stay on your credit report for:

- 7 years for negative accounts (like missed payments)

- 10 years for positive, paid-off accounts

However, if the account was closed in error or includes incorrect information, you can dispute it with the credit bureaus.

Is it better to pay off debt or save money first?

Ideally, do both, but it depends on your situation. Start by building an emergency fund (even $500 helps) so you don’t rely on credit for surprise expenses. Then focus on high-interest debt, like credit cards.

Use a method like the debt snowball (smallest balance first), debt avalanche (highest interest first), or my favorite the debt nor’easter to make steady progress.

Conclusion: Empowering Yourself for Financial Resilience

Credit setbacks can happen to anyone, even the most careful among us. But what matters most is how you respond.

Let’s recap the steps you can take:

- Understand what happened by reviewing your credit reports and identifying the issue.

- Take quick action by disputing errors and contacting creditors directly.

- Rebuild your credit with on-time payments, low credit utilization, and smart credit use.

- Use the right tools like credit monitoring apps, budgeting platforms, and educational resources.

- Stay proactive with regular financial check-ups and a commitment to learning.

The road back might feel long, but each smart step you take builds momentum. And every payment, every corrected error, every dollar saved is proof that you’re moving forward.

Having navigated my own financial challenges, I know how tough it can be, but I also know the freedom and confidence that come with taking control.

You’ve got this.